sentiment.csv

美國消費者信心指數

代碼:

from __future__ import absolute_import, division, print_function

# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost

import sys

import os

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

import matplotlib.pylab as plt

import seaborn as sns

# 一些配置項

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

sns.set(style='ticks', context='poster')

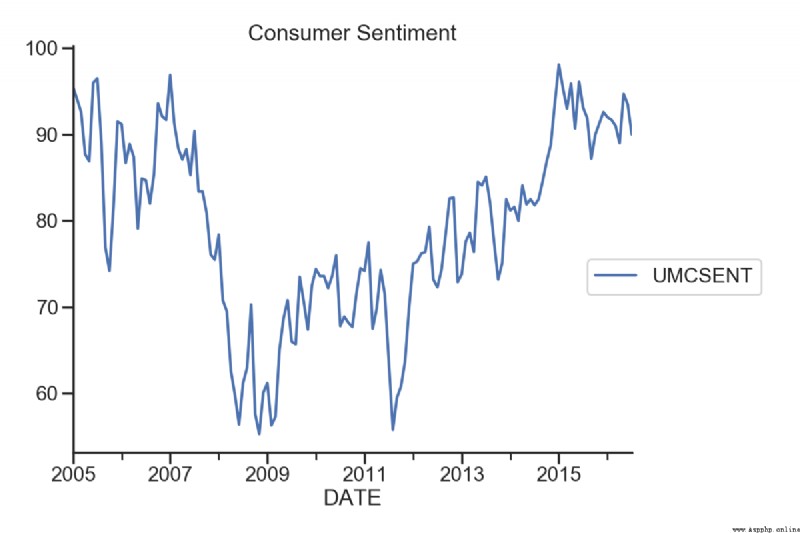

# 美國消費者信心指數

Sentiment = 'E:/file/sentiment.csv'

Sentiment = pd.read_csv(Sentiment, index_col=0, parse_dates=[0])

sentiment_short = Sentiment.loc['2005':'2016']

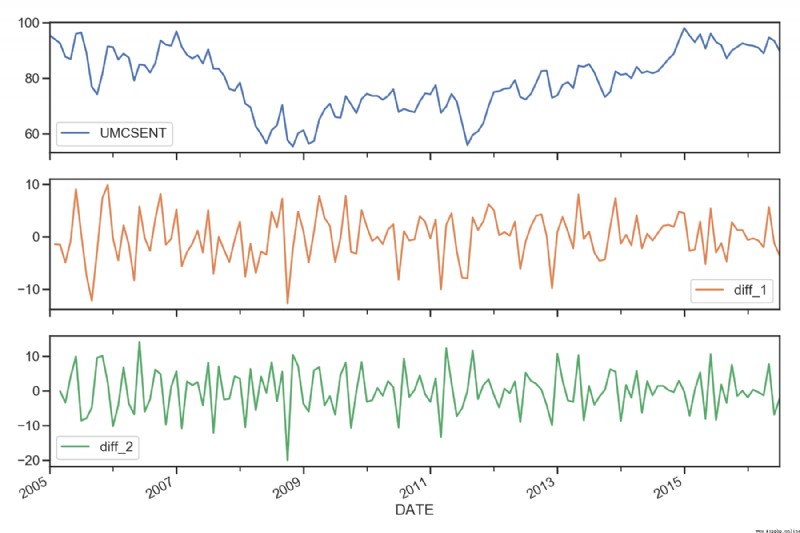

sentiment_short.plot(figsize=(12,8))

plt.legend(bbox_to_anchor=(1.25, 0.5))

plt.title("Consumer Sentiment")

sns.despine()

sentiment_short['diff_1'] = sentiment_short['UMCSENT'].diff(1)

sentiment_short['diff_2'] = sentiment_short['diff_1'].diff(1)

sentiment_short.plot(subplots=True, figsize=(18, 12))

del sentiment_short['diff_2']

del sentiment_short['diff_1']

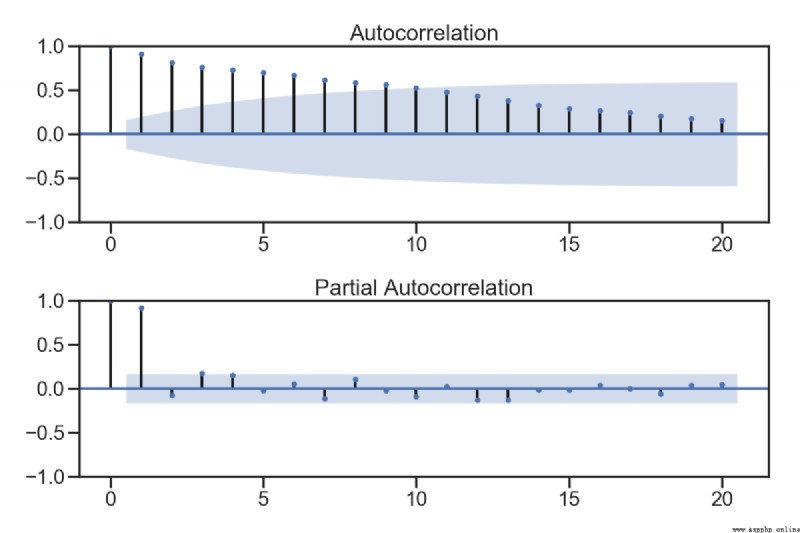

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(sentiment_short, lags=20,ax=ax1)

ax1.xaxis.set_ticks_position('bottom')

fig.tight_layout();

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(sentiment_short, lags=20, ax=ax2)

ax2.xaxis.set_ticks_position('bottom')

fig.tight_layout();

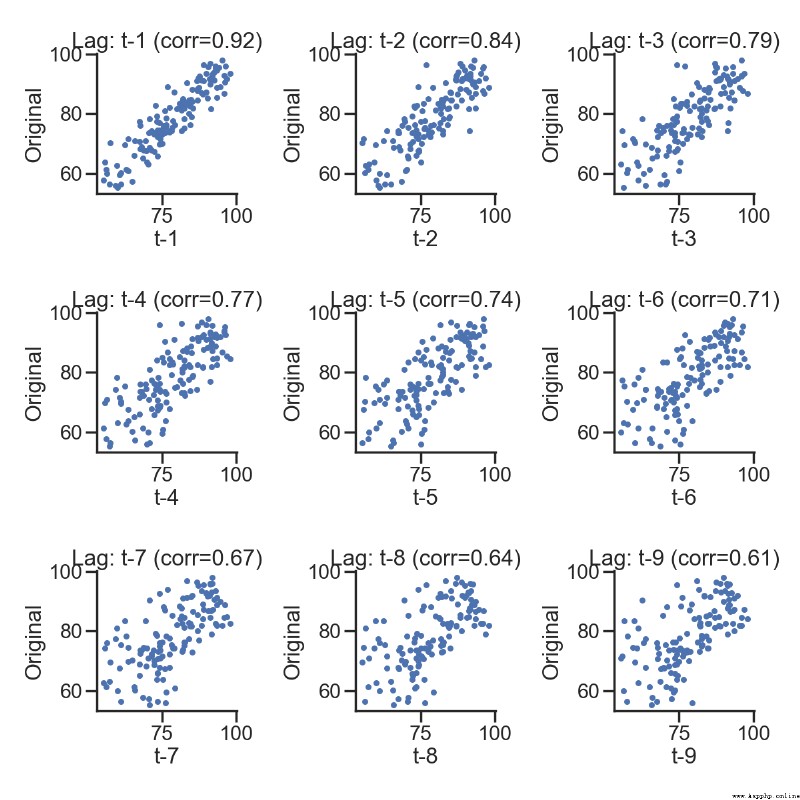

# 散點圖也可以表示

lags=9

ncols=3

nrows=int(np.ceil(lags/ncols))

fig, axes = plt.subplots(ncols=ncols, nrows=nrows, figsize=(4*ncols, 4*nrows))

for ax, lag in zip(axes.flat, np.arange(1,lags+1, 1)):

lag_str = 't-{}'.format(lag)

X = (pd.concat([sentiment_short, sentiment_short.shift(-lag)], axis=1,

keys=['y'] + [lag_str]).dropna())

X.plot(ax=ax, kind='scatter', y='y', x=lag_str);

corr = X.corr().iloc[:,:].values[0][1]

ax.set_ylabel('Original')

ax.set_title('Lag: {} (corr={:.2f})'.format(lag_str, corr));

ax.set_aspect('equal');

sns.despine();

fig.tight_layout();

# 更直觀一些

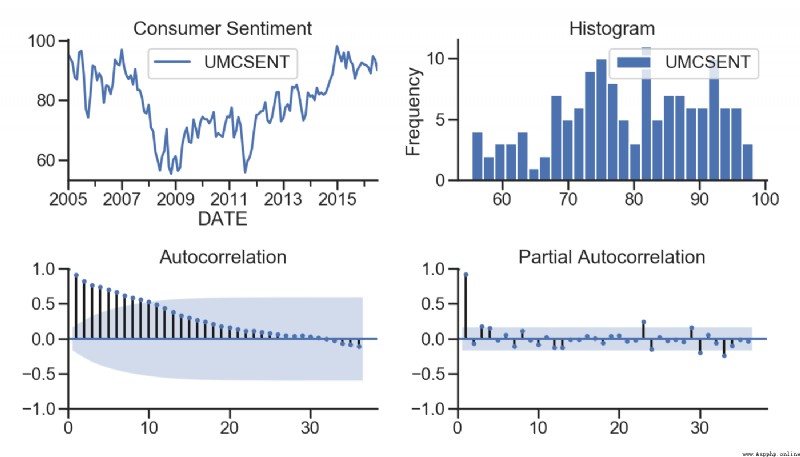

def tsplot(y, lags=None, title='', figsize=(14, 8)):

fig = plt.figure(figsize=figsize)

layout = (2, 2)

ts_ax = plt.subplot2grid(layout, (0, 0))

hist_ax = plt.subplot2grid(layout, (0, 1))

acf_ax = plt.subplot2grid(layout, (1, 0))

pacf_ax = plt.subplot2grid(layout, (1, 1))

y.plot(ax=ts_ax)

ts_ax.set_title(title)

y.plot(ax=hist_ax, kind='hist', bins=25)

hist_ax.set_title('Histogram')

smt.graphics.plot_acf(y, lags=lags, ax=acf_ax)

smt.graphics.plot_pacf(y, lags=lags, ax=pacf_ax)

[ax.set_xlim(0) for ax in [acf_ax, pacf_ax]]

sns.despine()

plt.tight_layout()

return ts_ax, acf_ax, pacf_ax

tsplot(sentiment_short, title='Consumer Sentiment', lags=36);

plt.show()

測試記錄:

代碼:

from __future__ import absolute_import, division, print_function

# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost

import sys

import os

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

import matplotlib.pylab as plt

import seaborn as sns

# 一些配置項

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

sns.set(style='ticks', context='poster')

# 讀取數據

Sentiment = 'E:/file/sentiment.csv'

Sentiment = pd.read_csv(Sentiment, index_col=0, parse_dates=[0])

sentiment_short = Sentiment.loc['2005':'2016']

# 自相關圖

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(sentiment_short, lags=20,ax=ax1)

ax1.xaxis.set_ticks_position('bottom')

fig.tight_layout();

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(sentiment_short, lags=20, ax=ax2)

ax2.xaxis.set_ticks_position('bottom')

fig.tight_layout();

plt.show()

測試記錄:

代碼:

from __future__ import absolute_import, division, print_function

# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost

import sys

import os

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

import matplotlib.pylab as plt

import seaborn as sns

# 一些配置項

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

sns.set(style='ticks', context='poster')

# 讀取數據

Sentiment = 'E:/file/sentiment.csv'

Sentiment = pd.read_csv(Sentiment, index_col=0, parse_dates=[0])

sentiment_short = Sentiment.loc['2005':'2016']

# 散點圖也可以表示

lags=9

ncols=3

nrows=int(np.ceil(lags/ncols))

fig, axes = plt.subplots(ncols=ncols, nrows=nrows, figsize=(4*ncols, 4*nrows))

for ax, lag in zip(axes.flat, np.arange(1,lags+1, 1)):

lag_str = 't-{}'.format(lag)

X = (pd.concat([sentiment_short, sentiment_short.shift(-lag)], axis=1,

keys=['y'] + [lag_str]).dropna())

X.plot(ax=ax, kind='scatter', y='y', x=lag_str);

corr = X.corr().iloc[:,:].values[0][1]

ax.set_ylabel('Original')

ax.set_title('Lag: {} (corr={:.2f})'.format(lag_str, corr));

ax.set_aspect('equal');

sns.despine();

fig.tight_layout();

plt.show()

測試記錄:

代碼:

from __future__ import absolute_import, division, print_function

# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost

import sys

import os

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

import matplotlib.pylab as plt

import seaborn as sns

# 一些配置項

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

sns.set(style='ticks', context='poster')

# 讀取數據

Sentiment = 'E:/file/sentiment.csv'

Sentiment = pd.read_csv(Sentiment, index_col=0, parse_dates=[0])

sentiment_short = Sentiment.loc['2005':'2016']

# 更直觀一些

def tsplot(y, lags=None, title='', figsize=(14, 8)):

fig = plt.figure(figsize=figsize)

layout = (2, 2)

ts_ax = plt.subplot2grid(layout, (0, 0))

hist_ax = plt.subplot2grid(layout, (0, 1))

acf_ax = plt.subplot2grid(layout, (1, 0))

pacf_ax = plt.subplot2grid(layout, (1, 1))

y.plot(ax=ts_ax)

ts_ax.set_title(title)

y.plot(ax=hist_ax, kind='hist', bins=25)

hist_ax.set_title('Histogram')

smt.graphics.plot_acf(y, lags=lags, ax=acf_ax)

smt.graphics.plot_pacf(y, lags=lags, ax=pacf_ax)

[ax.set_xlim(0) for ax in [acf_ax, pacf_ax]]

sns.despine()

plt.tight_layout()

return ts_ax, acf_ax, pacf_ax

tsplot(sentiment_short, title='Consumer Sentiment', lags=36);

plt.show()

測試記錄:

series1.csv

一個標准的時間序列數據

代碼:

from __future__ import absolute_import, division, print_function

# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost

import sys

import os

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

import matplotlib.pylab as plt

import seaborn as sns

# 一些配置項

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

sns.set(style='ticks', context='poster')

# 美國消費者信心指數

filename_ts = 'E:/file/series1.csv'

ts_df = pd.read_csv(filename_ts, index_col=0, parse_dates=[0])

n_sample = ts_df.shape[0]

# 劃分測試集和訓練集

n_train=int(0.95*n_sample)+1

n_forecast=n_sample-n_train

#ts_df

ts_train = ts_df.iloc[:n_train]['value']

ts_test = ts_df.iloc[n_train:]['value']

#print(ts_train.shape)

#print(ts_test.shape)

#print("Training Series:", "\n", ts_train.tail(), "\n")

#print("Testing Series:", "\n", ts_test.head())

def tsplot(y, lags=None, title='', figsize=(14, 8)):

fig = plt.figure(figsize=figsize)

layout = (2, 2)

ts_ax = plt.subplot2grid(layout, (0, 0))

hist_ax = plt.subplot2grid(layout, (0, 1))

acf_ax = plt.subplot2grid(layout, (1, 0))

pacf_ax = plt.subplot2grid(layout, (1, 1))

y.plot(ax=ts_ax)

ts_ax.set_title(title)

y.plot(ax=hist_ax, kind='hist', bins=25)

hist_ax.set_title('Histogram')

smt.graphics.plot_acf(y, lags=lags, ax=acf_ax)

smt.graphics.plot_pacf(y, lags=lags, ax=pacf_ax)

[ax.set_xlim(0) for ax in [acf_ax, pacf_ax]]

sns.despine()

fig.tight_layout()

return ts_ax, acf_ax, pacf_ax

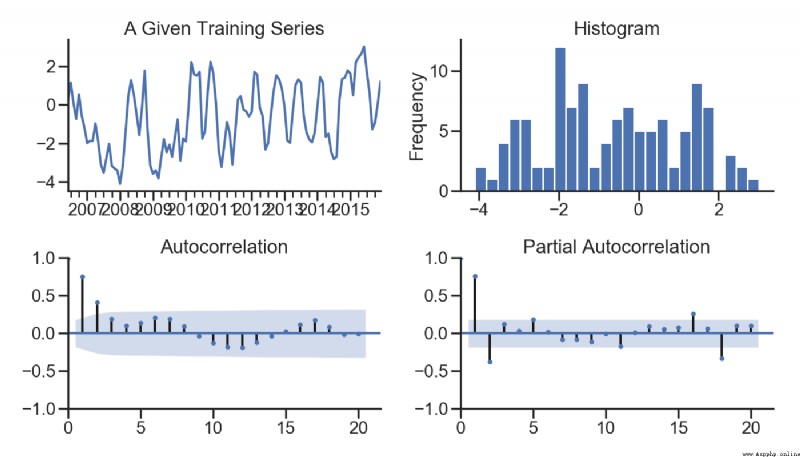

tsplot(ts_train, title='A Given Training Series', lags=20);

plt.show()

測試記錄:

代碼:

from __future__ import absolute_import, division, print_function

# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost

import sys

import os

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

import matplotlib.pylab as plt

import seaborn as sns

import itertools

# 一些配置項

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

sns.set(style='ticks', context='poster')

# 美國消費者信心指數

filename_ts = 'E:/file/series1.csv'

ts_df = pd.read_csv(filename_ts, index_col=0, parse_dates=[0])

n_sample = ts_df.shape[0]

# 劃分訓練集和測試集

n_train=int(0.95*n_sample)+1

n_forecast=n_sample-n_train

#ts_df

ts_train = ts_df.iloc[:n_train]['value']

ts_test = ts_df.iloc[n_train:]['value']

# 訓練模型

arima200 = sm.tsa.SARIMAX(ts_train, order=(2,0,0))

model_results = arima200.fit()

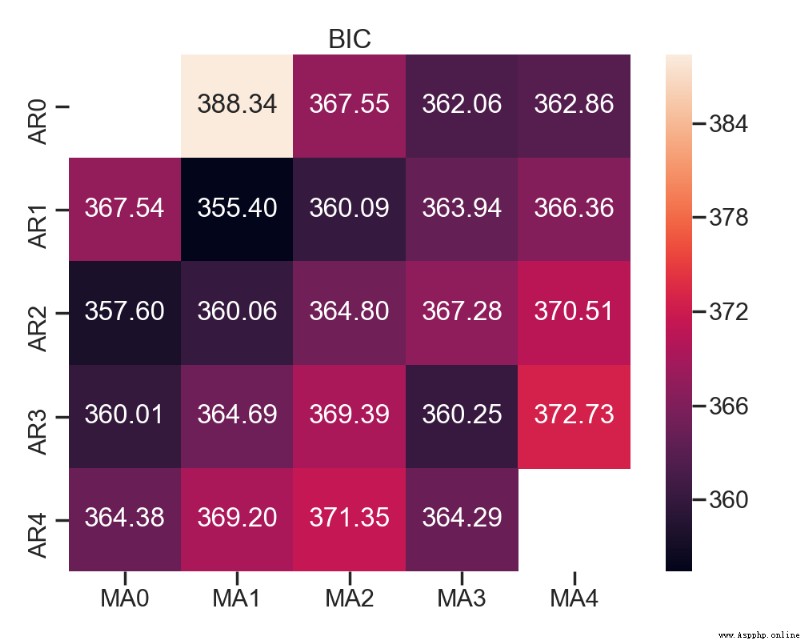

# 選擇參數

p_min = 0

d_min = 0

q_min = 0

p_max = 4

d_max = 0

q_max = 4

# Initialize a DataFrame to store the results

results_bic = pd.DataFrame(index=['AR{}'.format(i) for i in range(p_min, p_max + 1)],

columns=['MA{}'.format(i) for i in range(q_min, q_max + 1)])

for p, d, q in itertools.product(range(p_min, p_max + 1),

range(d_min, d_max + 1),

range(q_min, q_max + 1)):

if p == 0 and d == 0 and q == 0:

results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = np.nan

continue

try:

model = sm.tsa.SARIMAX(ts_train, order=(p, d, q),

# enforce_stationarity=False,

# enforce_invertibility=False,

)

results = model.fit()

results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = results.bic

except:

continue

results_bic = results_bic[results_bic.columns].astype(float)

fig, ax = plt.subplots(figsize=(10, 8))

ax = sns.heatmap(results_bic,

mask=results_bic.isnull(),

ax=ax,

annot=True,

fmt='.2f',

);

ax.set_title('BIC');

plt.show()

測試記錄:

代碼:

from __future__ import absolute_import, division, print_function

# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost

import sys

import os

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

import matplotlib.pylab as plt

import seaborn as sns

import itertools

# 一些配置項

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

sns.set(style='ticks', context='poster')

# 美國消費者信心指數

filename_ts = 'E:/file/series1.csv'

ts_df = pd.read_csv(filename_ts, index_col=0, parse_dates=[0])

n_sample = ts_df.shape[0]

# 劃分訓練集和測試集

n_train=int(0.95*n_sample)+1

n_forecast=n_sample-n_train

#ts_df

ts_train = ts_df.iloc[:n_train]['value']

ts_test = ts_df.iloc[n_train:]['value']

# 訓練模型

arima200 = sm.tsa.SARIMAX(ts_train, order=(2,0,0))

model_results = arima200.fit()

# AIC 和 BIC

#print(help(sm.tsa.arma_order_select_ic))

train_results = sm.tsa.arma_order_select_ic(ts_train, ic=['aic', 'bic'], trend='n', max_ar=4, max_ma=4)

print('AIC', train_results.aic_min_order)

print('BIC', train_results.bic_min_order)

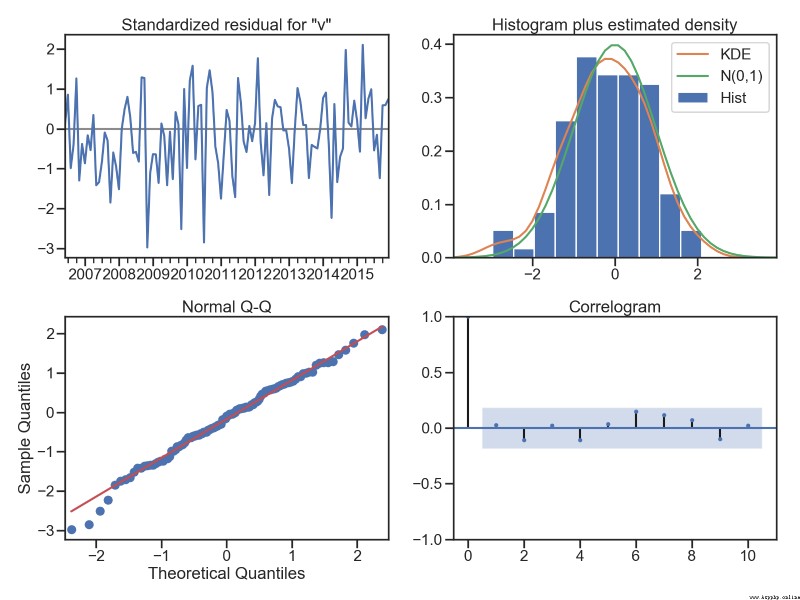

#殘差分析 正態分布 QQ圖線性

model_results.plot_diagnostics(figsize=(16, 12));

plt.show()

測試記錄:

AIC (3, 3)

BIC (1, 1)