7. Python quantitative trading - single moving average strategy upgrade 2: moving average cumulative calculation

編輯:Python

Catalog

Preface

The realization of cumulative computing

One 、 modify ma20 by list

Two 、 Strategy upgrade

3、 ... and 、 Histogram and k Line graph

Four 、 Complete source code

Preface

Last one , We have added to the regression strategy T+0 The limitation of , Next, let's add the cumulative calculation below the moving average

The realization of cumulative computing

1、 Below the moving average ,close < ma20 The number of times should reach a certain amount ( understand : The stock has fallen for a short time , Instead of buying as soon as we fall )

2、 Below the moving average ,close - ma20 The cumulative value should be large enough

One 、 modify ma20 by list

def __init__(self, strategy_name):

self._strategy_name = strategy_name

self._Dt = [] # Trading hours

self._Open = [] # Opening price

self._High = [] # Highest price

self._Low = [] # The lowest price

self._Close = [] # The latest price

self._Volume = []

self._tick = [] # data

self._last_bar_start_minute = None # Last update bar Time for

self._is_new_bar = False # Whether there are new bar

self._ma20 = []

self._ma20.insert(0, None)

self._close_minus_ma20 = np.zeros(20) # close - minus Of list

# Current order ,dict, Dictionaries

self._current_orders = {

}

# Historical orders

self._history_orders = {

}

self._order_number = 0

self._init = False # for backtesting

Two 、 Strategy upgrade

self._close_minus_ma20 < 0).sum() > 10: The number of falls exceeded 10 Time

self._close_minus_ma20.sum() / self._Close[1] < -0.02:ma20 Synthesis is negative , And fell more than the closing price 2%

def strategy(self):

# last < 0.95 *ma20 ,long position( Position ), last > ma20 *1.05, sell

if self._is_new_bar:

self._ma20.insert(1, sum(self._Close[1:21]) / 20)

self._close_minus_ma20[2:] = self._close_minus_ma20[1:len(self._close_minus_ma20) - 1]

self._close_minus_ma20[1] = self._Close[1] - self._ma20[1]

if 0 == len(self._current_orders):

if self._Close[0] < 0.98 * self._ma20[1]:

if (self._close_minus_ma20 < 0).sum() > 10 and self._close_minus_ma20.sum() / self._Close[1] < -0.02:

# 100000/44.28 = 2258 44.28 Is the current price ,10 The money you have

# 2258 -> 2200 shares

volume = int(100000 / self._Close[0] / 100) * 100

self._buy(self._Close[0] + 0.01, volume) # there 0.01 In order to prevent pending orders , We can buy whatever we need

elif 1 == len(self._current_orders):

if self._Close[0] > self._ma20[1] * 1.02:

key = list(self._current_orders.keys())[0]

if self._Dt[0].date() != self._current_orders[key]['open_datetime'].date():

self._sell(key, self._Close[0] - 0.01)

print('open date is %s, close date is: %s.'

% (self._history_orders[key]['open_datetime'].date(), self._Dt[0].date()))

else:

# if sam dates, sell order aborted due to T+0 limit

print('sell order aborted due to T+0 limit')

else: # len() = 2

raise ValueError("we have more then 1 current orders")

# Close[0] in between 0.95*ma20 and 1.05*ma20,do nothing

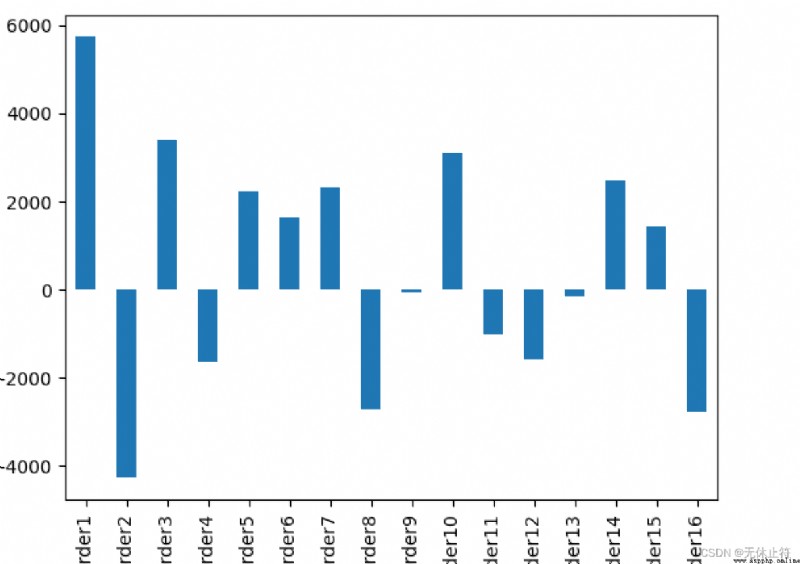

3、 ... and 、 Histogram and k Line graph

Result analysis : Although the idea is good , But in the actual intraday rate of return fell , So the strategy still needs to be adjusted

①.pnl Less , only 8200

②.order Less , only 16 single

Four 、 Complete source code

import requests

from time import sleep

from datetime import datetime, time, timedelta

from dateutil import parser

import pandas as pd

import numpy as np

import os

import matplotlib.pyplot as plt

# import mplfinance as mpf

from mplfinance.original_flavor import candlestick_ohlc

from matplotlib.dates import date2num

def get_ticks_for_backtesting(tick_path, bar_path):

""" :func: get ticks for backtesting, need two params :param1 tick_path: Generated backtest data path csv file with tick data, when there is not tick data, use bat_path to create tick data example: "E:\\Downloads\\600036_data\\600036_ticks.csv" :param2 bar_path: Of historical data tick route csv file with bar data, used in creating tick data example: "E:\\Downloads\\600036_data\\600036_5m.csv" :return: ticks in list with tuples in it, such as [(datetime, last_price), (datetime, last_price)] """

if os.path.exists(tick_path): # If back test data already exists , Read back test data directly ticks

ticks = pd.read_csv(

tick_path,

parse_dates=['datetime'],

index_col='datetime'

)

tick_list = []

for index, row in ticks.iterrows():

tick_list.append((index, row[0]))

# ticks = np.array(tick_list)

ticks = tick_list

else:

bar_5m = pd.read_csv(bar_path) # Use pandas Read csv data

ticks = []

for index, row in bar_5m.iterrows(): # Set the step size according to different opening prices

if row['open'] < 30:

step = 0.01

elif row['open'] < 60:

step = 0.03

elif row['open'] < 90:

step = 0.05

else:

step = 0.1

# in case of np.arrange(30, 30.11, 0.02), (open, high, step)

# we will not have 30.11 as the highest price,

# we might not catch high when step is more than 0.01

# that is why me need: arr = np.append(arr, row['high']) and

# arr = np.append(arr, row['low'])

arr = np.arange(row['open'], row['high'], step) # Generate from... In steps open To high The data of

arr = np.append(arr, row['high']) # This is to make up for the missing step size high

arr = np.append(arr, np.arange(row['open'] - step, row['low'], -step)) # Generate from... In steps open To low The data of

arr = np.append(arr, row['low']) # This is to make up for the missing step size low

arr = np.append(arr, row['close'])

i = 0

dt = parser.parse(row['datetime']) - timedelta(minutes=5)

for item in arr:

ticks.append((dt + timedelta(seconds=0.1 * i), item)) # Simulate the data time to 0.1 Second progressive

i += 1

tick_df = pd.DataFrame(ticks, columns=['datetime', 'price'])

tick_df.to_csv(tick_path, index=0) # Save to csv Back test data

return ticks

# __init__, structure , initialization , Instantiation

class AstockTrading(object):

""" :class: A stock trading platform, needs one param, It has backtesting, paper trading, and real trading. :param1: strategy_name: strategy_name """

def __init__(self, strategy_name):

self._strategy_name = strategy_name

self._Dt = [] # Trading hours

self._Open = [] # Opening price

self._High = [] # Highest price

self._Low = [] # The lowest price

self._Close = [] # The latest price

self._Volume = []

self._tick = [] # data

self._last_bar_start_minute = None # Last update bar Time for

self._is_new_bar = False # Whether there are new bar

self._ma20 = []

self._ma20.insert(0, None)

self._close_minus_ma20 = np.zeros(20) # close - minus Of list

# Current order ,dict, Dictionaries

self._current_orders = {

}

# Historical orders

self._history_orders = {

}

self._order_number = 0

self._init = False # for backtesting

def get_tick(self):

""" :func: for paper trading or real trading, not for backtesting It goes to sina to get last tick info, address is: https://hq.sinajs.cn/list=sh600519, sh600519 can be changed need to set headers Referer to: https://finance.sina.com.cn A The opening time of the shares is 9:15,9:15-9:25 It's call auction -> Opening price ,9:25 9:25-9:30 Don't trade , Time >9:30, The deal begins start this method after 9:25 tick info is organized in tuple, such as (trade_datetime, last_price), tick info is save in self._tick. :param: no param :return: None """

headers = {

'Referer': "https://finance.sina.com.cn"}

page = requests.get("https://hq.sinajs.cn/list=sh600519", headers=headers)

stock_info = page.text

mt_info = stock_info.replace("\"", "").split("=")[1].split(",")

# The latest price

last = float(mt_info[1])

trade_datetime = mt_info[30] + ' ' + mt_info[31]

self._tick = (trade_datetime, last)

def get_history_data_from_local_machine(self):

""" :not done yet :return: """

# tushare Data sources

# self.Open = [1, 2, 3]

# self.High = [2, 3, 4]

self._Open = []

self._High = []

self._Low = []

self._Close = []

self._Dt = []

def bar_generator(self):

""" :not done yet :how save and import history data? :return: """

# assume we have history data already

# 1、update bars,calculate 5 minutes ma20 , not daily data

# 2、compare last and ma20 -> buy or sell or pass

# assume we have history data,Open,High,Low,Close,Dt

# This could be 5minutes、10minutes、15minutes、20minutes、30minutes

if self._tick[0].minute % 5 == 0 and self._tick[0].minute != self._last_bar_start_minute:

self._last_bar_start_minute = self._tick[0].minute

self._Open.insert(0, self._tick[1])

self._High.insert(0, self._tick[1])

self._Low.insert(0, self._tick[1])

self._Close.insert(0, self._tick[1])

self._Dt.insert(0, self._tick[0])

self._is_new_bar = True

else:

# update current bar

self._High[0] = max(self._High[0], self._tick[1])

self._Low[0] = max(self._Low[0], self._tick[1])

self._Close[0] = self._tick[1]

self._Dt[0] = self._tick[0]

self._is_new_bar = False

def _buy(self, price, volume):

""" :method: create am order :param1 price: buying price :param2 volume: buying volume :return: none """

self._order_number += 1

key = "order" + str(self._order_number)

self._current_orders[key] = {

"open_datetime": self._Dt[0],

"open_price": price,

"volume": volume # Number of shares

}

pass

def _sell(self, key, price):

""" :method: close a long order, It needs two params :param1 key: long order's key :param2 price: selling price :return: """

self._current_orders[key]['close_price'] = price

self._current_orders[key]['close_datetime'] = self._Dt[0]

self._current_orders[key]['pnl'] = \

(price - self._current_orders[key]['open_price']) \

* self._current_orders[key]['volume'] \

- price * self._current_orders[key]['volume'] * 1 / 1000 \

- (price - self._current_orders[key]['open_price']) \

* self._current_orders[key]['volume'] * 3 / 10000

# move order from current orders to history orders

self._history_orders[key] = self._current_orders.pop(key)

def strategy(self):

# last < 0.95 *ma20 ,long position( Position ), last > ma20 *1.05, sell

if self._is_new_bar:

self._ma20.insert(1, sum(self._Close[1:21]) / 20)

self._close_minus_ma20[2:] = self._close_minus_ma20[1:len(self._close_minus_ma20) - 1]

self._close_minus_ma20[1] = self._Close[1] - self._ma20[1]

if 0 == len(self._current_orders):

if self._Close[0] < 0.98 * self._ma20[1]:

if (self._close_minus_ma20 < 0).sum() > 10 and self._close_minus_ma20.sum() / self._Close[1] < -0.02:

# 100000/44.28 = 2258 44.28 Is the current price ,10 The money you have

# 2258 -> 2200 shares

volume = int(100000 / self._Close[0] / 100) * 100

self._buy(self._Close[0] + 0.01, volume) # there 0.01 In order to prevent pending orders , We can buy whatever we need

elif 1 == len(self._current_orders):

if self._Close[0] > self._ma20[1] * 1.02:

key = list(self._current_orders.keys())[0]

if self._Dt[0].date() != self._current_orders[key]['open_datetime'].date():

self._sell(key, self._Close[0] - 0.01)

print('open date is %s, close date is: %s.'

% (self._history_orders[key]['open_datetime'].date(), self._Dt[0].date()))

else:

# if sam dates, sell order aborted due to T+0 limit

print('sell order aborted due to T+0 limit')

else: # len() = 2

raise ValueError("we have more then 1 current orders")

# Close[0] in between 0.95*ma20 and 1.05*ma20,do nothing

def bar_generator_for_backtesting(self, tick):

""" :method: for backtesting only, used to update _Open, _ High, etc, It needs just one param :param tick: tick info in tuple, (datetime, price) :return: """

if tick[0].minute % 5 == 0 and tick[0].minute != self._last_bar_start_minute:

self._last_bar_start_minute = tick[0].minute

self._Open.insert(0, tick[1])

self._High.insert(0, tick[1])

self._Low.insert(0, tick[1])

self._Close.insert(0, tick[1])

self._Dt.insert(0, tick[0])

self._is_new_bar = True

else:

# update current bar

self._High[0] = max(self._High[0], tick[1])

self._Low[0] = max(self._Low[0], tick[1])

self._Close[0] = tick[1]

self._Dt[0] = tick[0]

self._is_new_bar = False

def run_backtestting(self, ticks):

""" :method: ticks will be used to generate bars, when bars is long enough, call strategy() :param ticks: list with (datetime, price) in the list :return: none """

for tick in ticks:

self.bar_generator_for_backtesting(tick)

if self._init:

self.strategy()

else:

if len(self._Open) >= 100:

self._init = True

self.strategy()

# ma = AstockTrading('600036') # Class instantiation

# ma.get_history_data_from_local_machine()

#

# # The trading time is 9:30-11:30,13:00-15:00

# while time(9, 26) < datetime.now().time() < time(11, 32) \

# or time(13) < datetime.now().time() < time(15, 2):

# ma.get_tick()

# ma.bar_generator()

# ma.strategy()

# # trade_time = parser.parse(ma._tick[0]).time()

# # sleep(3)

if __name__ == '__main__':

tick_path = "E:\\Downloads\\600036_data\\600036_ticks.csv"

bar_path = "E:\\Downloads\\600036_data\\600036_5m.csv"

ticks = get_ticks_for_backtesting(tick_path, bar_path) # Get back test data

ast = AstockTrading('ma')

ast.run_backtestting(ticks) # Run back test data

print('ast._current_orders:')

print(ast._current_orders)

print("-------------------------------------")

print('ast._history_orders:')

print(ast._history_orders)

# Use matplotlib Draw a profit and loss histogram

profit_orders = 0 # Number of profitable transactions

loss_orders = 0 # Number of loss making transactions

orders = ast._history_orders

for key in orders.keys():

if orders[key]['pnl'] >= 0:

profit_orders += 1

else:

loss_orders += 1

win_rate = profit_orders / len(orders)

loss_rate = loss_orders / len(orders)

# T = transpose

orders_df = pd.DataFrame(orders).T

orders_df.loc[:, 'pnl'].plot.bar()

plt.show()

# print sum of pnl

print('sum of pnl is: ' + str(orders_df.loc[:, 'pnl'].sum()))

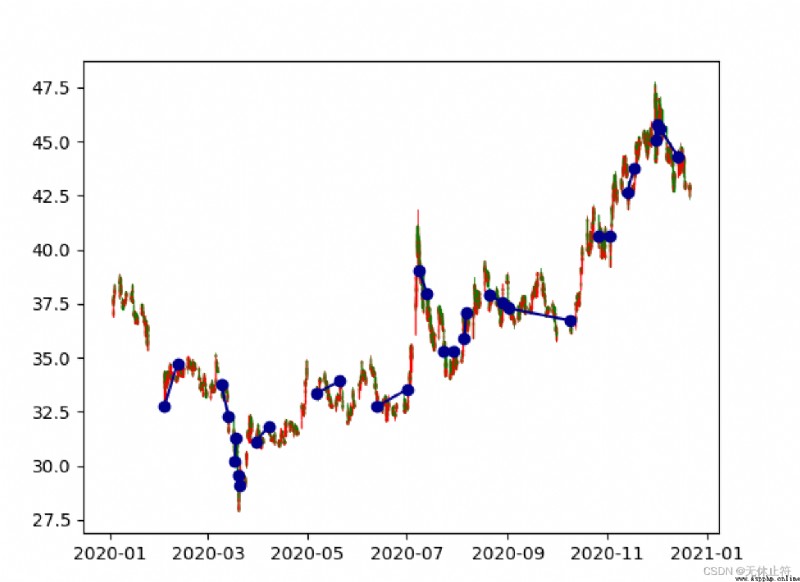

# Use mplfinance draw k Line graph : Order transaction price and time

bar5 = pd.read_csv(bar_path, parse_dates=['datetime'])

bar5.loc[:, 'datetime'] = [date2num(x) for x in bar5.loc[:, 'datetime']]

fig, ax = plt.subplots()

candlestick_ohlc(

ax,

quotes=bar5.values,

width=0.2,

colorup="r",

colordown='g',

alpha=1.0,

)

# put orders in candle sticks

for index, row in orders_df.iterrows():

ax.plot(

[row['open_datetime'], row['close_datetime']],

[row['open_price'], row['close_price']],

color='darkblue',

marker='o',

)

plt.show()